Microfinance Opportunities (MFO) and Financial Sector Deepening Zambia (FSDZ) are pleased to announce the release of the Zambia Financial Diaries: Interim Report. The report presents initial insights and findings from the study including:

- A simple income segmentation framework that shows that people with higher week-to-week variation in their income are more likely to use a financial tool other than home savings to manage their money.

- An analysis of spending, which shows:

- Respondents tended to finance large, lump sum expenditures out of their cash flow rather than through the use of a financial tool such a loan or savings, and

- Respondents with low week-to-week variation in their income were more likely to make lump sum expenditures

- The high priority the respondents placed on the purchase of airtime

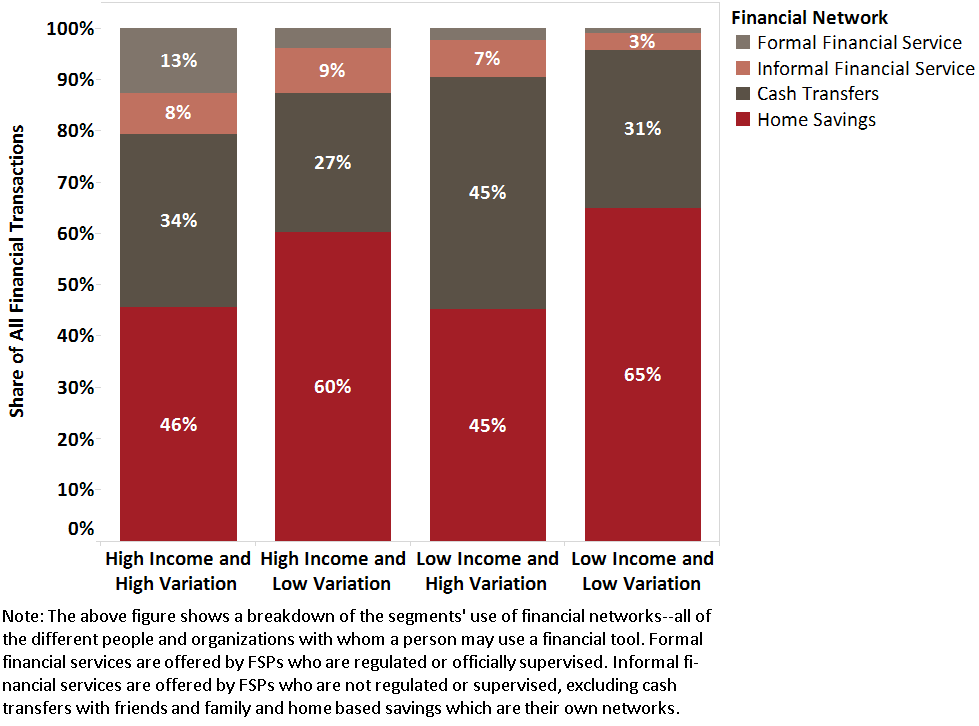

- An analysis of respondents’ financial service use, which shows that most respondents were financially excluded, relying on home savings and cash transfers from friends and family to manage their cash flow.

The report discusses the implications of these early insights for financial service providers (FSPs) and policy makers. A full copy of the report can be found here.

In November 2014, FSDZ commissioned MFO to conduct a yearlong study to gather weekly data on all transactions performed by a sample of low-income respondents in Zambia. This report draws on data from the mid-point of the study and includes 50,000 transactions collected from 352 respondents in the Lusaka, Copperbelt, Eastern, and Western Provinces.

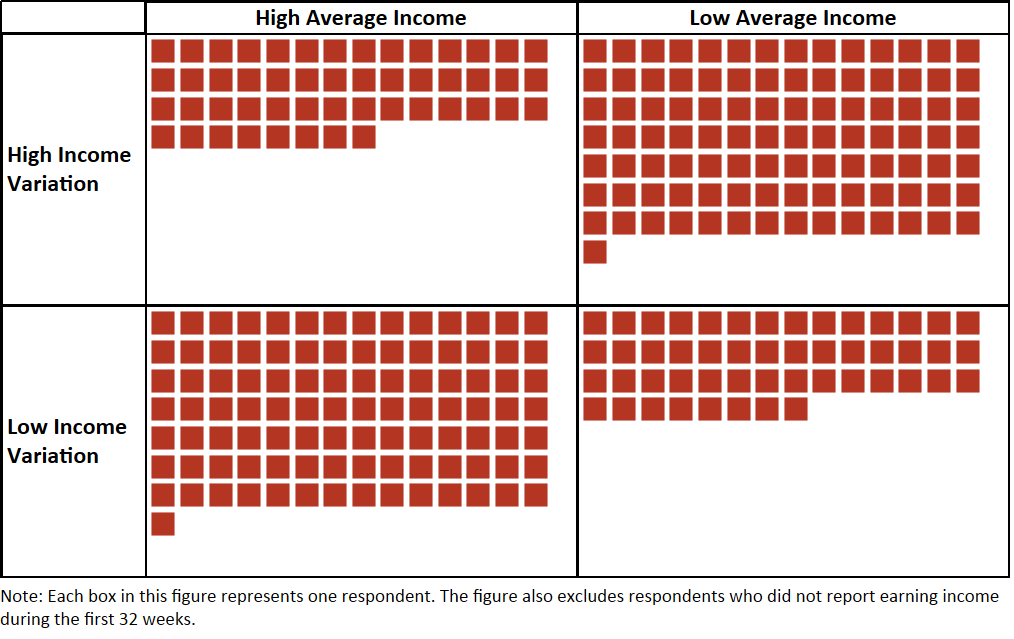

The report carefully examines respondents’ sources of income. It shows that the number of sources varied significantly from respondent to respondent as did the extent to which they relied on their principal source of income. Smallholder farmers, for instance, earned income from four different sources on average, and salaried workers often had at least two income sources.

The report also shows that understanding respondents’ demographic and socio-economic characteristics is a necessary but insufficient condition for understanding their financial service use. Understanding respondents’ cash flow patterns is also important. To that end, this report suggests a simple framework to segment low-income individuals and households based on their income patters, specifically their income level and the degree of week-to-week variation in their income. The report describes how these two dimensions of economic behavior are strongly associated with financial service use. For example, respondents with higher income variation relied less on home savings than those with lower income variation.

Figure 1: Income Segmentation Framework

Figure 2: Financial Service Use by Income Segment

The report also looks closely at respondents’ expenditures. It shows that a majority of expenditures were devoted to buying food and household products, such as candles and washing powder, and that these expenditures occurred in informal markets. Respondents spent very little on discretionary items such as entertainment or alcohol. Respondents spent a notable amount on airtime, which was the most common type of transaction after food and household products, suggesting the importance of communication for low-income individuals. Using the income segmentation framework, the report shows that respondents with lower weekly income variation were more likely to make lump sum purchases than those with higher weekly income variation.

Finally, the report looks at the financial networks that the respondents tapped into to manage their money. The data suggest that they were financially excluded. During the period of the study they relied predominantly on home savings and cash transfers from family and friends to help meet their financial needs. Furthermore, looking at financial tool use through the income segmentation framework shows that individuals with higher income variation relied on financial tools more often than their low variation peers.

The early findings from the Zambia Financial Diaries provide three major insights for FSPs and policy makers. First, they reveal the need for FSPs and policy-makers in Zambia to focus on the behavior of low-income individuals and households rather than just their socio-economic and demographic characteristics. Doing this prior to developing new initiatives or financial products should help avoid inefficiencies in efforts to promote financial inclusion. Second, the findings show that respondents’ spending behavior is concentrated at informal locations which could be potential touch-points to reach consumers with new marketing campaigns and products. Third, the findings remind FSPs and policy makers about the prominence of home savings and informal cash transfer networks among families and with friends in Zambia. While mobile operators have already started offering cash transfer options, revisiting tariff structures and marketing to people based on their economic behaviors may be a way to refine these products.

Please stay tuned for future updates from the Zambia Financial Diaries. If you are interested in discussing these findings or have any questions for our researchers, please feel free to contact us at [email protected].